Introduction

Building a strong credit history is essential for financial stability, but many people struggle to find an easy and affordable way to improve their credit scores. Kikoff is a credit-building tool designed to help users establish and grow their credit with minimal effort and cost. Unlike traditional credit cards or loans, Kikoff offers a unique, low-risk way to improve your credit profile without high fees or interest charges.

Whether you’re just starting your credit journey or looking to rebuild your score, Kikoff provides a simple and effective solution. In this guide, we’ll explore how Kikoff works, its benefits, and how it compares to other credit-building tools.

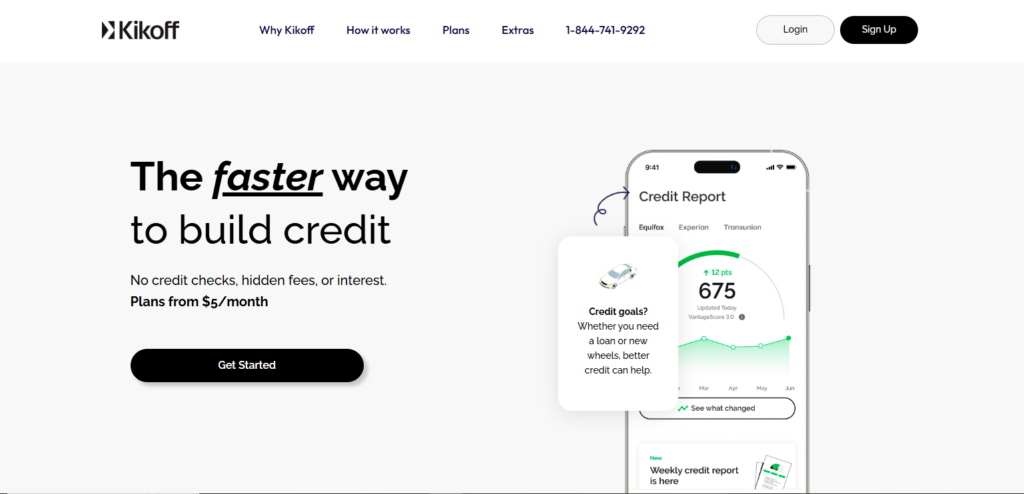

The faster way to build credit

No credit checks, hidden fees, or interest.

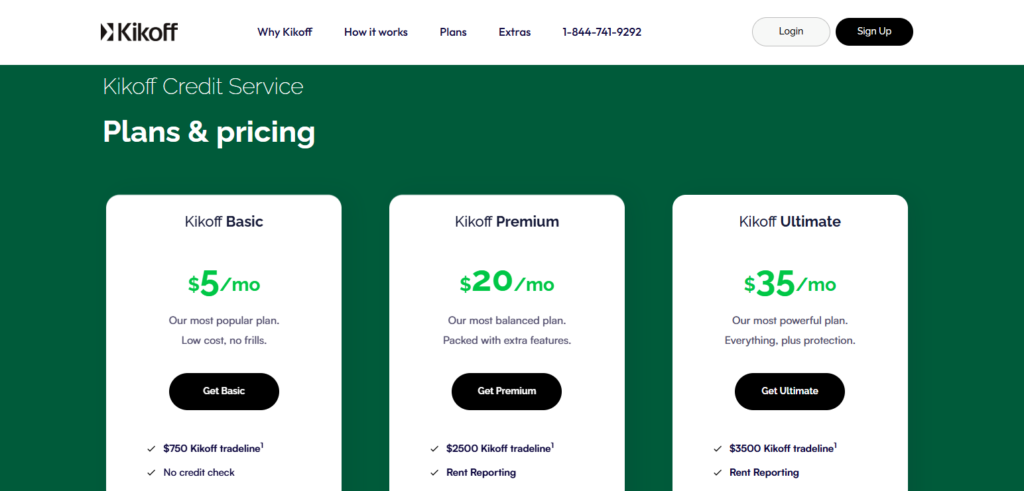

Plans from $5/month

What is Kikoff?

Kikoff is a credit-building platform designed to help users improve their credit scores easily and affordably. It offers a revolving credit line with no interest, no hidden fees, and no credit check required, making it an ideal option for those new to credit or looking to rebuild their financial standing.

When you sign up for Kikoff, you get access to a Kikoff Credit Account, which reports to major credit bureaus like Equifax and Experian. This account functions as a small line of credit, typically used to make purchases from the Kikoff Store, which sells digital financial and self-improvement products. By making on-time payments, users can build positive credit history over time.

Unlike traditional credit cards or personal loans, Kikoff is structured to minimize risk while maximizing credit growth potential. It does not require a security deposit, and there are no hard credit checks, making it accessible to almost anyone.

Pricing & Fees

One of the biggest advantages of Kikoff is its affordability. Unlike traditional credit-building options that come with high fees and interest rates, Kikoff offers a cost-effective way to improve your credit score.

Currently, Kikoff provides a Kikoff Credit Account with a $5 monthly membership fee. This account grants access to a revolving credit line, which is reported to major credit bureaus like Equifax and Experian. The best part? There are no interest charges, late fees, or hidden costs.

In addition to the Kikoff Credit Account, the platform also offers a Kikoff Credit Builder Loan, which requires a one-time fee (instead of monthly payments). This product is designed for users who want to diversify their credit profile further.

Compared to competitors, Kikoff stands out for its transparent pricing and lack of extra charges, making it an excellent choice for those who want to build credit without the risk of accumulating debt.

Credit-Building Effectiveness

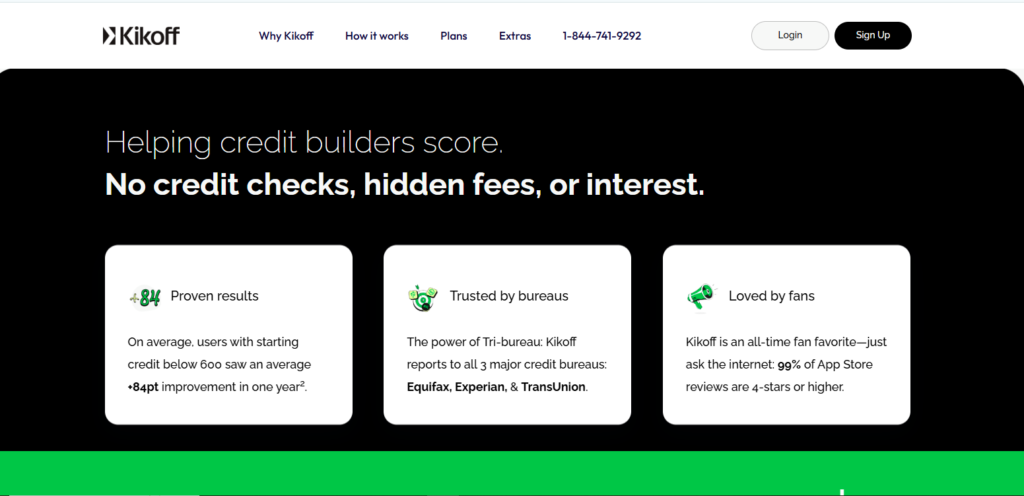

The main goal of Kikoff is to help users build and improve their credit scores efficiently. Since payment history makes up 35% of your FICO score, consistently making on-time payments with Kikoff can have a significant positive impact on your credit profile.

Kikoff reports to major credit bureaus, including Equifax and Experian, which means your account activity contributes to your overall credit history. Many users have reported seeing an increase in their credit scores within a few months of responsible use.

Another key advantage of Kikoff is that it helps improve your credit utilization ratio—a critical factor in determining your credit score. By maintaining a low balance on your Kikoff Credit Account, you can demonstrate responsible credit usage, which can lead to a higher credit score over time.

Unlike traditional credit cards, Kikoff does not charge interest or require a credit check, making it a low-risk option for those who are new to credit or trying to rebuild their scores.

Credit Bureau Reporting

One of the key factors that make Kikoff an effective credit-building tool is its credit bureau reporting. Kikoff reports your account activity to major credit bureaus, including Equifax and Experian, ensuring that your responsible credit usage contributes to your overall credit profile.

Since payment history is the most important factor in determining your credit score, making on-time payments to Kikoff can help you establish a positive credit history. Over time, this can lead to a higher credit score, making it easier to qualify for loans, credit cards, or even better interest rates.

However, it’s important to note that Kikoff does not currently report to TransUnion. While this may limit its impact slightly, reporting to Equifax and Experian still provides a strong foundation for credit improvement.

By consistently using Kikoff and keeping your balance low, you can demonstrate responsible credit behavior, which is essential for long-term financial growth.

Competitor Comparison

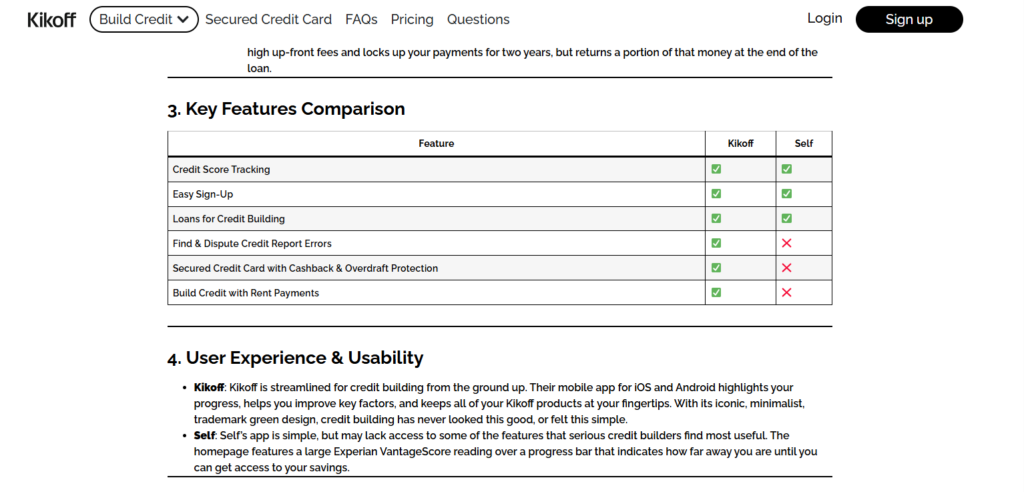

When choosing a credit-building tool, it’s important to compare Kikoff with other popular options to determine which one best fits your needs. While Kikoff is known for its affordability and ease of use, other credit-building services like Self, Credit Strong, and Chime Credit Builder offer different features that may appeal to certain users.

Kikoff vs. Self

- Kikoff charges a $5 monthly fee with no interest, while Self offers credit builder loans that require monthly payments ranging from $25 to $150.

- Self reports to all three credit bureaus (Equifax, Experian, and TransUnion), whereas Kikoff reports to Equifax and Experian only.

Kikoff vs. Credit Strong

- Credit Strong focuses on installment credit builder loans, which require larger monthly payments, while Kikoff offers a revolving credit line with more flexibility.

- Kikoff is more budget-friendly, whereas Credit Strong’s plans start at $15 per month.

Kikoff vs. Chime Credit Builder

- Chime Credit Builder requires a Chime checking account and works like a secured credit card, whereas Kikoff does not require a bank account or security deposit.

- Both services charge no interest or annual fees, making them affordable options for credit building.

Which One is Best for You?

- If you prefer a low-cost, easy-to-use option with no hard credit check, Kikoff is a great choice.

- If you want a credit builder loan and can commit to higher monthly payments, Self or Credit Strong may be better.

- If you’re looking for a secured card alternative, Chime Credit Builder could be a good fit.

Pros & Cons of Kikoff

Like any credit-building tool, Kikoff has its advantages and drawbacks. Understanding the pros and cons of Kikoff can help you decide if it’s the right choice for improving your credit score.

Pros of Kikoff

✅ No Interest or Hidden Fees – Unlike traditional credit cards, Kikoff does not charge interest, late fees, or annual fees. The only cost is the $5 monthly membership fee.

✅ No Credit Check Required – Kikoff is accessible to anyone, regardless of their credit history, since there are no hard credit checks during sign-up.

✅ Reports to Major Credit Bureaus – Payments are reported to Equifax and Experian, helping users build a positive credit history.

✅ Flexible & Easy to Use – Unlike credit builder loans, Kikoff offers a revolving credit line, allowing users to make small purchases and improve their credit utilization.

✅ Low-Cost Credit-Building Solution – At just $5 per month, Kikoff is one of the most affordable ways to establish or rebuild credit.

Cons of Kikoff

❌ Does Not Report to TransUnion – While Kikoff reports to Equifax and Experian, it does not currently report to TransUnion, which may limit its impact on your overall credit profile.

❌ Purchases Limited to Kikoff Store – The credit line can only be used for purchases in the Kikoff Store, which sells financial and self-improvement products.

❌ No Instant Credit Score Boost – Like all credit-building tools, Kikoff takes time to show results. Users typically see credit score improvements after a few months of consistent use.

Is Kikoff Right for You?

If you’re looking for an affordable, low-risk way to build credit, Kikoff is a great option. However, if you need a credit card that can be used anywhere or a service that reports to all three bureaus, you may want to consider alternatives.

Who Should Use Kikoff?

Kikoff is designed for individuals looking to build or improve their credit scores without taking on high-interest debt. Whether you are just starting your credit journey or trying to rebuild your financial profile, Kikoff offers a simple and affordable solution.

Best for Beginners with No Credit History

If you are new to credit and want to establish a solid credit foundation, Kikoff provides an easy entry point. With no credit check required, you can start building credit immediately without worrying about being denied.

Ideal for Those Repairing Their Credit

For individuals with a low or damaged credit score, Kikoff can help demonstrate responsible credit behavior by reporting on-time payments to Equifax and Experian. This makes it a great tool for credit recovery after financial setbacks.

Helpful for Those Who Want a Low-Cost Option

Unlike traditional credit cards or credit builder loans, Kikoff only charges a $5 monthly fee with no interest, late fees, or hidden charges. This makes it perfect for those who want to build credit affordably.

Not Ideal for Those Who Need a Usable Credit Card

Since the Kikoff Credit Account can only be used for purchases in the Kikoff Store, it may not be suitable for those looking for a general-purpose credit card. If you need a credit line for everyday spending, a secured credit card or traditional credit card may be a better choice.

Final Verdict: Is Kikoff Worth It?

If you’re looking for a simple, low-cost way to build or improve your credit score, Kikoff is definitely worth considering. With no interest, no hard credit check, and a $5 monthly fee, it’s one of the most affordable credit-building tools available.

For credit beginners and those with poor credit, Kikoff provides an easy way to establish positive payment history and improve credit utilization. It reports to Equifax and Experian, which can help boost your credit score over time. However, the fact that it does not report to TransUnion may limit its impact for some users.

One potential downside is that Kikoff’s credit line can only be used in its own store, making it less flexible than traditional credit cards or secured cards. If you need a credit card for everyday spending, a secured credit card may be a better choice.

Who Should Use Kikoff?

- Best for: Credit newbies, individuals with poor credit, and those looking for a low-risk way to build credit.

- Not ideal for: People who need a usable credit card for everyday purchases.

Bottom Line

If your goal is to build credit affordably and you don’t mind the spending restrictions, Kikoff is a great option. With responsible use, it can help you increase your credit score and open the door to better financial opportunities.