Introduction

Building credit is an essential part of financial health, but it can be challenging if you’re starting from scratch or trying to recover from past credit issues. This is where Kikoff comes in. As a credit-building tool, Kikoff is designed to help users establish or improve their credit scores with a low-cost, interest-free approach. But does it really work?

In this detailed Kikoff reviews guide, we’ll explore everything you need to know about the platform, including how it works, pricing, pros and cons, credit bureau reporting, and real user experiences. By the end, you’ll have a clear idea of whether Kikoff is the right choice for you.

What is Kikoff and How Does It Work?

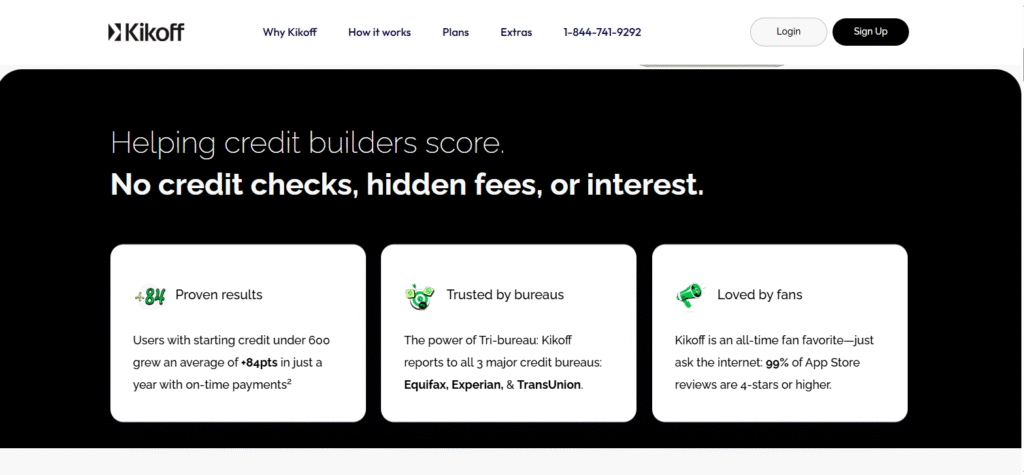

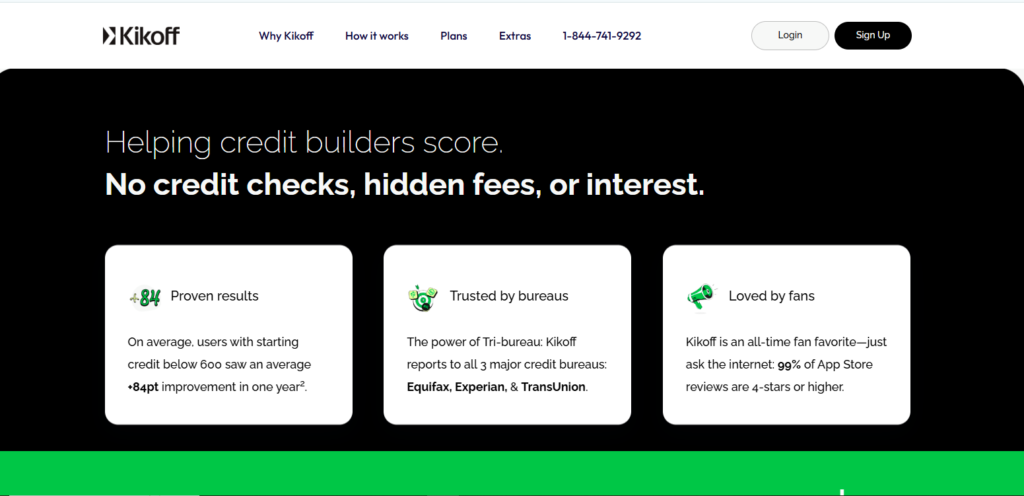

Kikoff is a credit-building service designed to help users improve their credit scores in an easy and affordable way. Unlike traditional credit cards, Kikoff offers a credit account with no interest, no hard credit check, and a low monthly fee. This makes it an attractive option for individuals who are new to credit or looking to repair their credit history.

How Does Kikoff Work?

Kikoff provides a credit line that users can access to make purchases within the Kikoff store, which sells digital financial education products. The goal is to create a history of on-time payments, which Kikoff then reports to major credit bureaus. Here’s how the process works:

- Signing up is simple, with instant approval and no hard credit check

- Users receive a small credit line to make purchases

- The credit can only be used in the Kikoff store to buy digital products

- Making small monthly payments helps establish positive credit activity

- Kikoff reports these payments to Experian and Equifax, helping users build credit over time

Since Kikoff has no interest or hidden fees, it’s a low-risk way to start building a credit history without taking on unnecessary debt.

Start with a plan,

skip the credit check

No credit checks. No hidden fees. No interest.

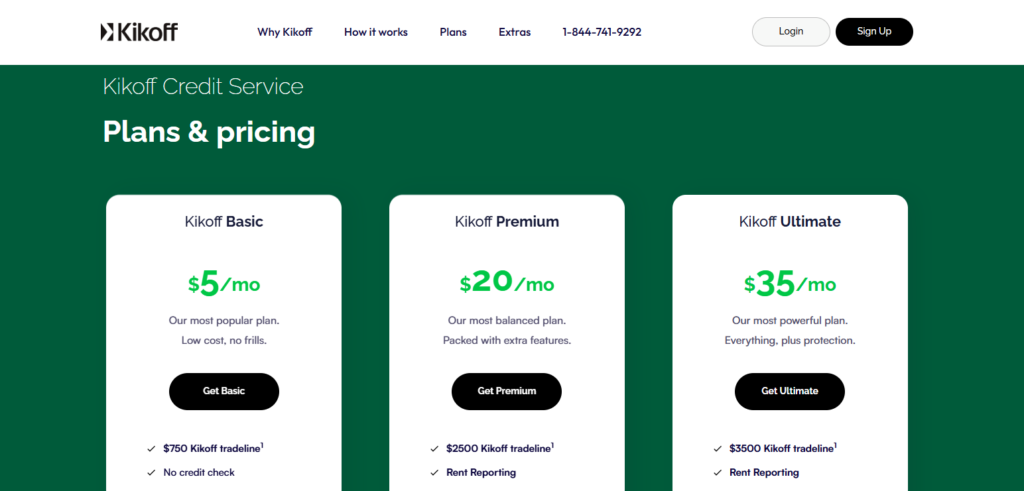

Kikoff Pricing & Membership Fees

One of the biggest advantages of Kikoff is its affordable pricing model, making it an accessible option for those looking to build credit without high costs. Unlike traditional credit-building options that charge interest, annual fees, or security deposits, Kikoff keeps things simple and budget-friendly.

Kikoff Membership Plans

Kikoff offers different plans, each designed to help users improve their credit score:

- Kikoff Credit Account – Costs $5 per month with no interest, no late fees, and no credit check. This plan provides a small credit line that can be used to make purchases within the Kikoff store.

- Kikoff Credit Builder Loan – A structured installment plan that helps build credit by making fixed monthly payments, which are then reported to credit bureaus.

There are no hidden fees or annual charges, making Kikoff a cost-effective solution for anyone looking to establish or improve their credit score.

Does Kikoff Really Help Build Credit?

For anyone looking to improve their credit score, Kikoff offers a simple and affordable way to build credit history. But does it actually work? The short answer is yes, as long as you use it responsibly.

How Kikoff Helps Build Credit

Kikoff is designed to establish positive credit habits by reporting on-time payments to major credit bureaus. This can have a significant impact on your credit score, especially if you are new to credit or trying to rebuild.

- Reports to Experian & Equifax – Monthly payments are sent to two major credit bureaus, helping users build a payment history.

- Improves Payment History – Since payment history makes up 35% of your credit score, making consistent payments can boost your score over time.

- Adds to Credit Age – The longer you keep your Kikoff account open, the more it positively impacts your credit age, which contributes to your overall score.

- No Hard Credit Check – Getting started won’t hurt your credit score, making it a risk-free option for credit-building.

Factors That Affect Results

While Kikoff can help improve your credit, results depend on individual factors:

- Consistently making on-time payments is crucial.

- Other existing debts and credit usage may affect how quickly your score improves.

- Kikoff works best when used alongside other responsible credit habits like keeping low credit utilization.

Credit Bureau Reporting: Who Does Kikoff Report To?

A key factor in determining whether Kikoff is effective for credit-building is its credit bureau reporting. When lenders and financial institutions assess creditworthiness, they rely on information from major credit bureaus. So, who exactly does Kikoff report to?

Which Credit Bureaus Receive Kikoff Reports?

Kikoff reports payment activity to two of the three major credit bureaus:

- Experian – One of the largest credit bureaus, used by many lenders to assess creditworthiness.

- Equifax – Another major bureau that tracks credit history and influences credit scores.

At this time, Kikoff does not report to TransUnion, which means some lenders may not see your Kikoff account on your credit report. However, since Experian and Equifax are widely used, Kikoff can still have a positive impact on most credit applications.

Why Credit Bureau Reporting Matters

- Helps Build a Positive Payment History – On-time payments reported to Experian and Equifax can boost your credit score over time.

- Establishes Credit for Beginners – If you’re new to credit, Kikoff provides an easy way to build history with major bureaus.

- Limited Impact Without TransUnion – Some lenders check all three bureaus, so Kikoff alone may not fully cover your credit profile.

User Experience & Platform Usability

One of the standout features of Kikoff is its user-friendly platform, designed for both beginners and experienced credit builders. Whether you access it via the mobile app or web dashboard, the interface is intuitive, simple, and easy to navigate.

App & Website Usability

- Clean & Minimalist Design – The app is well-organized, making it easy to track payments, check balances, and view credit progress.

- Seamless Sign-Up Process – Users can create an account in minutes, with no hard credit check required.

- Smooth Navigation – Essential features like payment tracking, credit line usage, and settings are easily accessible.

Customer Support & Assistance

- Responsive Support – Users can get help through email support and an in-app help center.

- Limited Contact Options – Unlike some competitors, Kikoff does not offer live chat or phone support, which could be a downside for users who prefer real-time assistance.

Kikoff vs. Competitors

When it comes to credit-building services, Kikoff competes with several platforms that offer similar features. Understanding how it compares can help you decide whether it’s the best option for your needs.

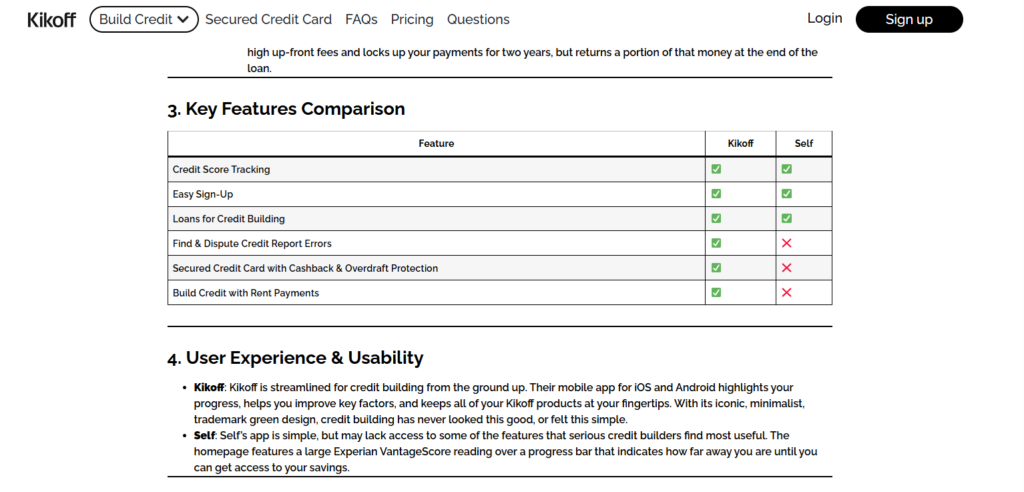

Kikoff vs. Self

- Pricing – Kikoff is more affordable, with plans starting at just $5 per month, while Self requires monthly payments toward a credit-builder loan.

- Credit Reporting – Both report to Experian and Equifax, but Self also reports to TransUnion, which may give it a slight edge.

- Ease of Use – Kikoff is simpler to use, while Self requires users to make loan payments over a set period.

Kikoff vs. Chime Credit Builder

- Eligibility – Chime requires a Chime checking account to qualify, while Kikoff is open to anyone.

- Fees – Kikoff has fixed, low-cost pricing, while Chime is fee-free but requires users to fund their own credit-building account.

- Credit Reporting – Both report to Experian and Equifax, but Chime also reports to TransUnion.

Kikoff vs. Credit Strong

- Credit-Building Approach – Kikoff offers a credit line, while Credit Strong uses a credit-builder loan that requires monthly payments.

- Cost – Kikoff is cheaper, while Credit Strong has higher fees due to its loan structure.

- Credit Impact – Both help establish payment history, but Credit Strong may be better for those looking to diversify their credit mix.

Key Takeaways

- Kikoff is one of the most affordable credit-building options.

- Unlike Chime and Self, Kikoff does not report to TransUnion.

- Competitors offer different credit-building methods, such as credit-builder loans, while Kikoff provides a revolving line of credit.

Pros & Cons Based on User Feedback

When evaluating Kikoff, it’s essential to look at real user experiences to understand the platform’s strengths and weaknesses. Based on customer reviews, here’s a breakdown of the pros and cons of using Kikoff for credit building.

Pros of Kikoff

- Affordable Credit-Building Solution – With plans starting as low as $5 per month, Kikoff is one of the most budget-friendly ways to improve credit.

- No Hard Credit Check – Signing up does not require a hard inquiry, making it accessible for those with poor or no credit history.

- Reports to Experian & Equifax – Payments are reported to two major credit bureaus, helping users establish positive payment history.

- Easy-to-Use Platform – The intuitive mobile app and website make tracking progress simple.

- No Interest Charges – Unlike traditional credit cards, Kikoff’s credit line comes with no interest, reducing financial burden.

Cons of Kikoff

- Does Not Report to TransUnion – Some lenders may not see your Kikoff account since it doesn’t report to all three major credit bureaus.

- Limited Credit Usage – The credit line can only be used for Kikoff’s digital store, limiting spending flexibility.

- No Phone or Live Chat Support – Customer service is email-based, which can result in delayed responses.

- May Take Time to See Results – While some users notice improvements within a few months, credit-building is a gradual process.

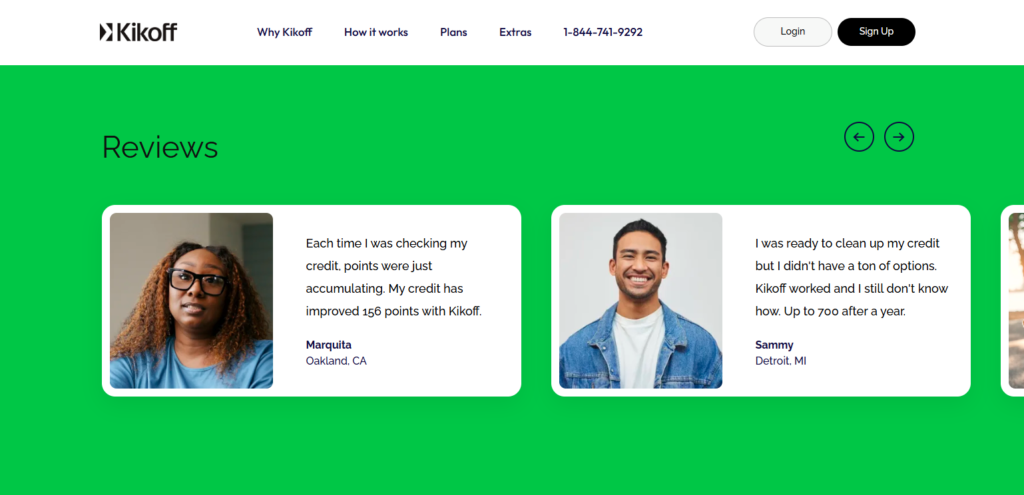

Real Customer Reviews & Success Stories

When choosing a credit-building service like Kikoff, it’s helpful to see what real users have to say. Many customers have shared their experiences—both positive and negative—about how Kikoff has impacted their credit scores and financial goals.

Positive User Experiences

Many users praise Kikoff for being an affordable and effective way to build credit. Here are some success stories:

- Fast Credit Score Increases – Some users report seeing their credit scores increase by 20-50 points within a few months of using Kikoff.

- Beginner-Friendly – Many first-time credit users appreciate how Kikoff provides a risk-free way to establish a credit history.

- No Hidden Fees – Customers like that Kikoff’s pricing is clear and predictable, without interest charges or surprise fees.

User Testimonial

“I signed up for Kikoff with no credit history, and within six months, my score went from 0 to 680! It was super easy to use, and I didn’t have to worry about fees or interest.” – James T.

Negative User Experiences

While Kikoff has many satisfied customers, some users mention downsides:

- Limited Spending Options – Some people are disappointed that the credit line can only be used for Kikoff’s digital store.

- Does Not Report to TransUnion – A few users wish Kikoff would report to all three major credit bureaus for maximum impact.

- Slow Customer Support – Some reviewers note that getting a response from Kikoff’s support team can take several days.

User Testimonial

“Kikoff helped me build my credit, but I wish I could use my credit line for other purchases. Also, their customer service is only available through email, which can be frustrating.” – Sarah M.

Final Verdict: Is Kikoff Worth It?

For those looking for a simple and affordable way to build credit, Kikoff can be a valuable tool. With no hard credit check, no interest, and a low monthly fee, it’s an excellent option for beginners or anyone needing to strengthen their credit profile.

Who Should Consider Kikoff?

- First-time credit users who need to establish credit history.

- Individuals with low or no credit who want to improve their score gradually.

- Anyone looking for a no-interest, low-cost credit-building solution.

Who Might Want to Look Elsewhere?

- Those who need a traditional credit card with broader spending options.

- People wanting a credit line that reports to all three bureaus (Kikoff only reports to Experian and Equifax).

- Users who prefer live customer support over email-based assistance.

Overall, Kikoff is worth considering if you need a risk-free, low-cost credit-building option. While it may not be a complete solution for everyone, it provides an easy and effective way to boost your credit score over time.